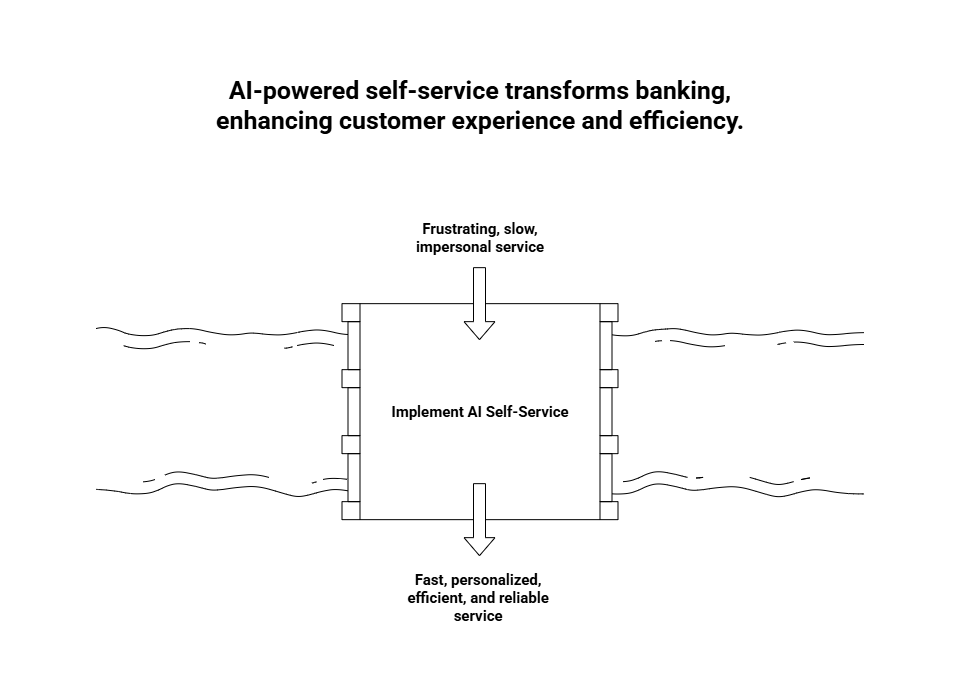

The banking world is going through a shift that’s hard to ignore. Customers don’t want to wait on calls, fill lengthy forms, or walk into branches unless they absolutely have to. What they do want is control—instant answers, smoother interactions, and the freedom to resolve simple issues on their own.

Digital-first banks understood this early. That’s why they’ve moved aggressively toward AI-powered self-service journeys that handle a massive portion of customer interactions without any human involvement.

Here’s the thing: this isn’t just a trend. It’s a complete redesign of how banking service works.

Let’s break down why this shift is happening, what AI is actually enabling, and how it’s changing the metrics banks care about most.

Customers Have Changed—And Banks Can’t Ignore It

For years, financial services leaned on physical touchpoints: branches, manual verification, call centers. But consumer behavior shifted faster than anyone predicted.

Today, people expect:

Instant updates

24/7 services

Fast authentication

Support without long conversations

Transparency and control over transactions

If a bank makes them wait—even 20 seconds—there’s irritation. If a process involves unnecessary steps, they abandon it. If support feels slow or complicated, they switch providers.

Digital-first banks realized something simple:

Self-service isn’t a “channel” anymore. It’s the experience.

AI moved it from being a set of FAQs and forms → to becoming a dynamic, intelligent, real-time assistant.

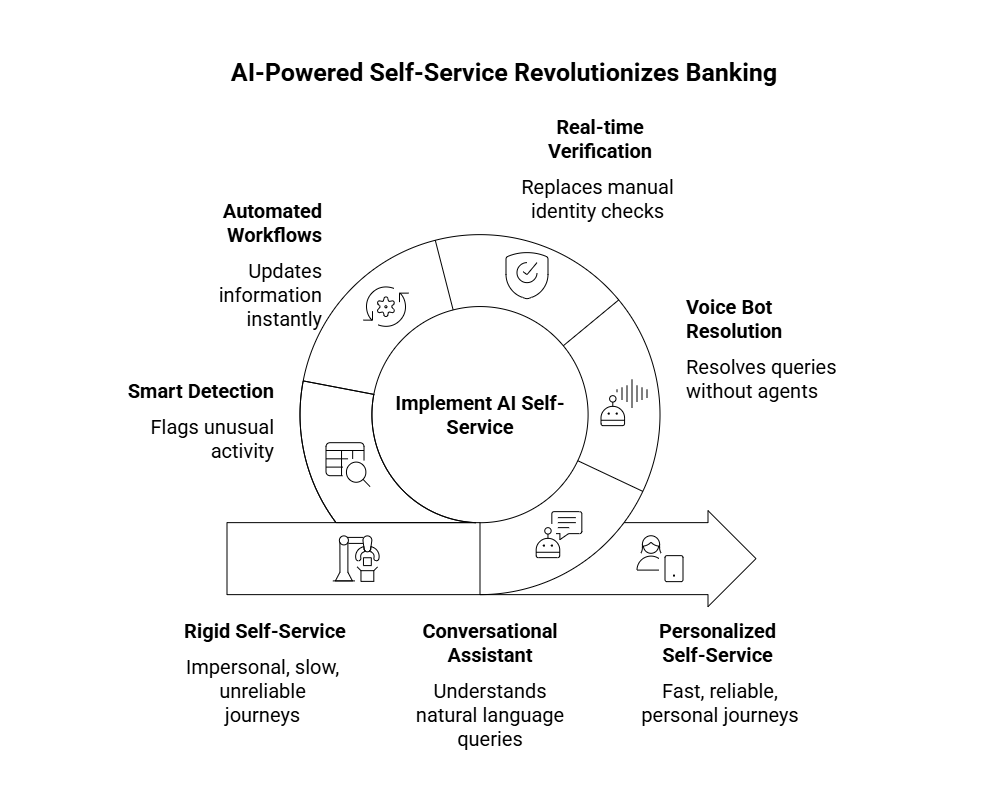

What AI-Powered Self-Service Actually Means

A lot of people talk about “AI self-service,” but let’s be clear about what’s happening behind the scenes.

AI is enabling journeys that feel personal, fast, and reliable.

Instead of a traditional bot that fails on basic questions, AI creates experiences like:

A conversational assistant that understands natural language

A voice bot that resolves queries without routing to an agent

Real-time verification that replaces manual checks

Automated workflows that update cards, limits, accounts, or loan info instantly

Smart detection that flags unusual activity and asks customers to confirm

The difference is night and day.

Old self-service = rigid menus.

AI self-service = “How can I help?” with actual understanding.

The Journeys Banks Are Now Automating

Digital-first banks are turning high-volume queries into self-service flows powered by AI and automation. These include:

Balance and transaction queries

No waiting. No IVR loops. Customers ask and get immediate clarity.

Card controls

Activate a card, freeze/unfreeze it, set limits—all without human involvement.

Loan eligibility and basic underwriting checks

AI screens inputs, pre-validates documents, and gives users an instant sense of what they qualify for.

Smart routing for complex needs

If a customer does need help, AI identifies the intent and routes them to the right specialized agent, not a generic queue.

Fraud alerts & confirmations

AI detects suspicious behaviors → contacts the customer instantly → asks for confirmation → updates the system.

KYC renewal & documentation support

Instead of back-and-forth emails and calls, the system guides customers through uploads and validations.

These aren’t small improvements. They directly attack the biggest pain points customers complain about.

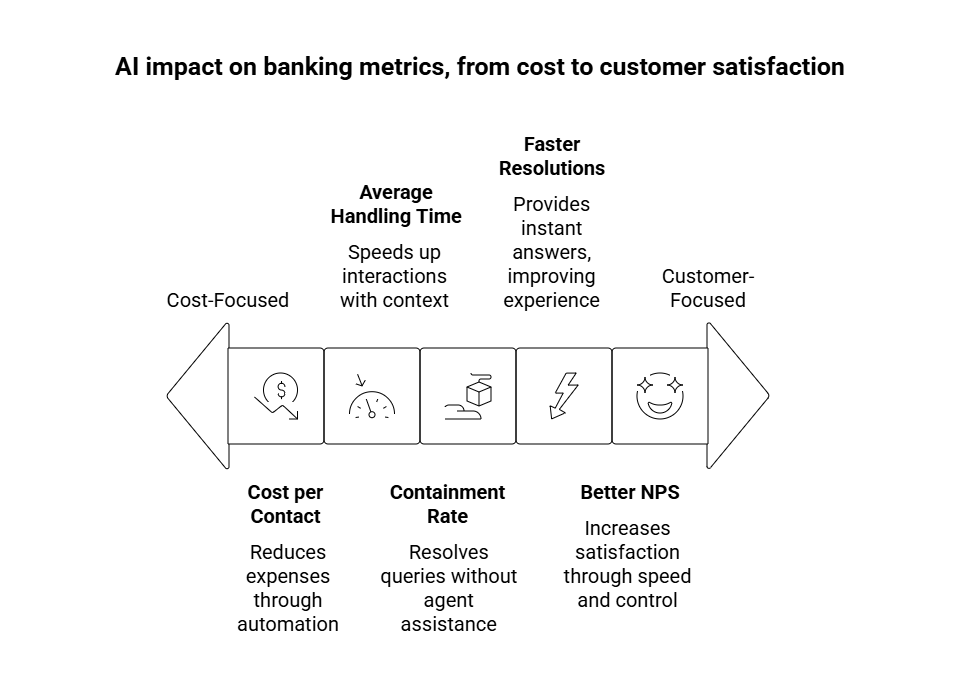

The Metrics That Make Banks Push Toward AI

Every bank watches a few core numbers:

Cost per contact

First-contact resolution

Average handling time (AHT)

Containment rate (how many queries never reach agents)

Customer lifetime value

Churn rate

AI touches all of these.

Lower cost per interaction

Automated journeys cost a fraction of an agent call.

Reduced AHT

AI collects context, pre-verifies information, and hands agents a complete picture—if escalation happens at all.

Higher containment rate

A smart bot resolves far more queries on its own than legacy IVR loops ever could.

Faster resolutions

Customers get what they need in seconds, not minutes.

Better NPS

People appreciate speed and control. AI gives them both.

This is exactly why digital-first banks, neobanks, and fintechs are scaling AI faster than traditional banks.

Why AI Self-Service Works Better for Banks Than “More Agents”

A common misconception:

If customers are unhappy, just hire more support staff.

But this model breaks down quickly.

More agents = higher cost with no guarantee of better service.

Traffic spikes during salary days, loan repayment cycles, fraud waves, or outages. No team can scale up and down at that speed.

AI is infinitely scalable.

AI never gets tired, stressed, or overloaded.

Whether you have 100 customers or 100,000 contacting at the same time, self-service journeys stay consistent.

AI systems learn over time.

Every interaction sharpens the model.

Agents don’t always retain or apply training consistently—but AI does.

That’s why digital-first banks rely on automated flows, not extra manpower.

The Technologies Powering These Self-Service Journeys

Behind the scenes, several layers of AI are working in sync:

NLP-based chatbots

They understand intent, context, past queries, and user profile data.

Voice AI for real-time recognition

Customers can talk naturally—no button presses required.

Automated verification systems

Identity checks, risk scoring, and document validation happen instantly.

Unified customer profiles

AI uses data from CRM and EHR-like banking records to personalize each interaction.

Predictive models

They anticipate issues before customers even raise them—like alerting them about unusual spending patterns.

The result is a system that feels intuitive instead of mechanical.

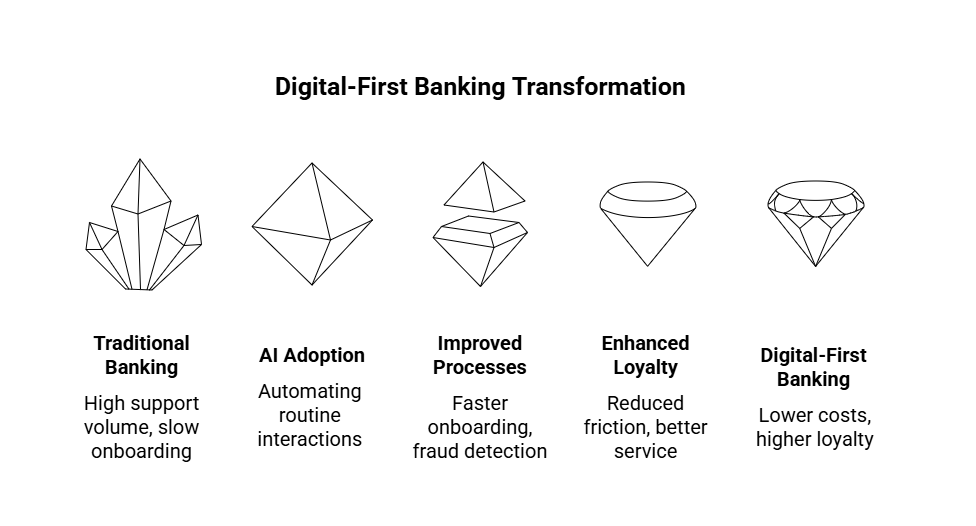

Where Digital-First Banks See the Biggest Wins

Digital-first banks aren’t adopting AI just because it’s “modern.” They’re doing it because the ROI is immediate and obvious.

Here’s what they get:

1. Massive reduction in support volume

Around 40–70% of routine banking interactions can be automated.

2. Faster onboarding & fewer drop-offs

AI guides the user through steps that normally cause confusion.

3. Stronger fraud detection & response

AI draws patterns that humans miss.

4. Higher customer loyalty

Self-service reduces friction—the number one reason people switch banks.

5. Lower operational costs

You don’t add headcount every time you scale your user base.

Traditional banks are realizing they need to catch up. Digital-only banks already have the head start.

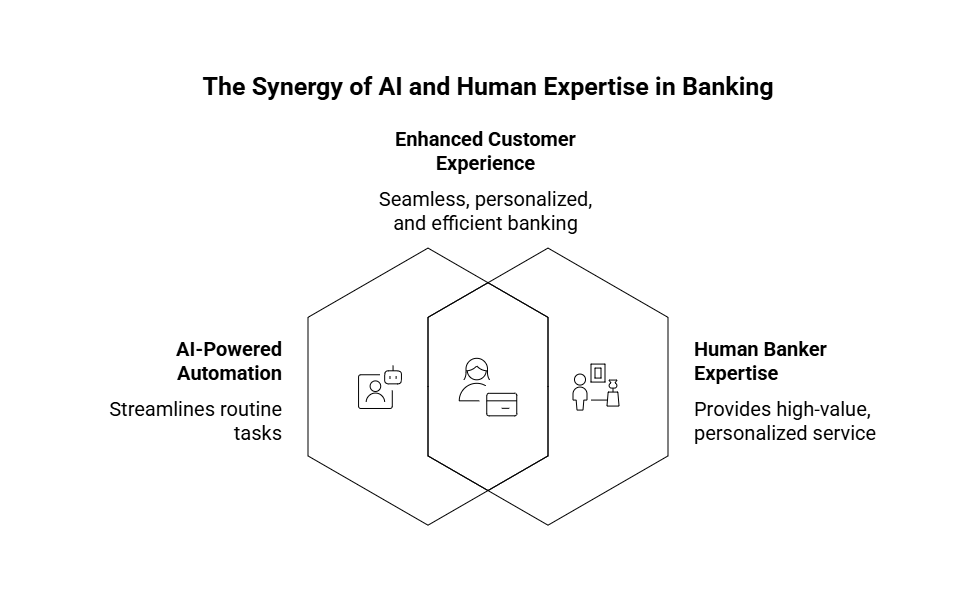

What This Means for the Future of Banking

AI isn’t replacing bankers.

It’s replacing friction.

Branches won’t vanish tomorrow, but their purpose will shift.

Agents won’t disappear, but they’ll focus on high-value work instead of resetting passwords or checking card statuses.

The future looks like this:

Hyper-personalized financial dashboards

Instant credit decisions

AI-driven investment guidance

Completely automated dispute handling

Proactive alerts based on behavior patterns

In short:

Banking becomes something customers “experience,” not something they “wait for.”

Final Thoughts

The move toward AI-powered self-service isn’t optional anymore. It’s the only scalable way to deliver fast, accurate, always-on banking that modern customers expect.

Digital-first banks knew this early, and they’re pulling ahead because of it.

Traditional banks now face a choice:

Adapt… or let customers drift to smarter alternatives.